W-2 vs. 1099: Compliance for Event Staff

December 18, 2025

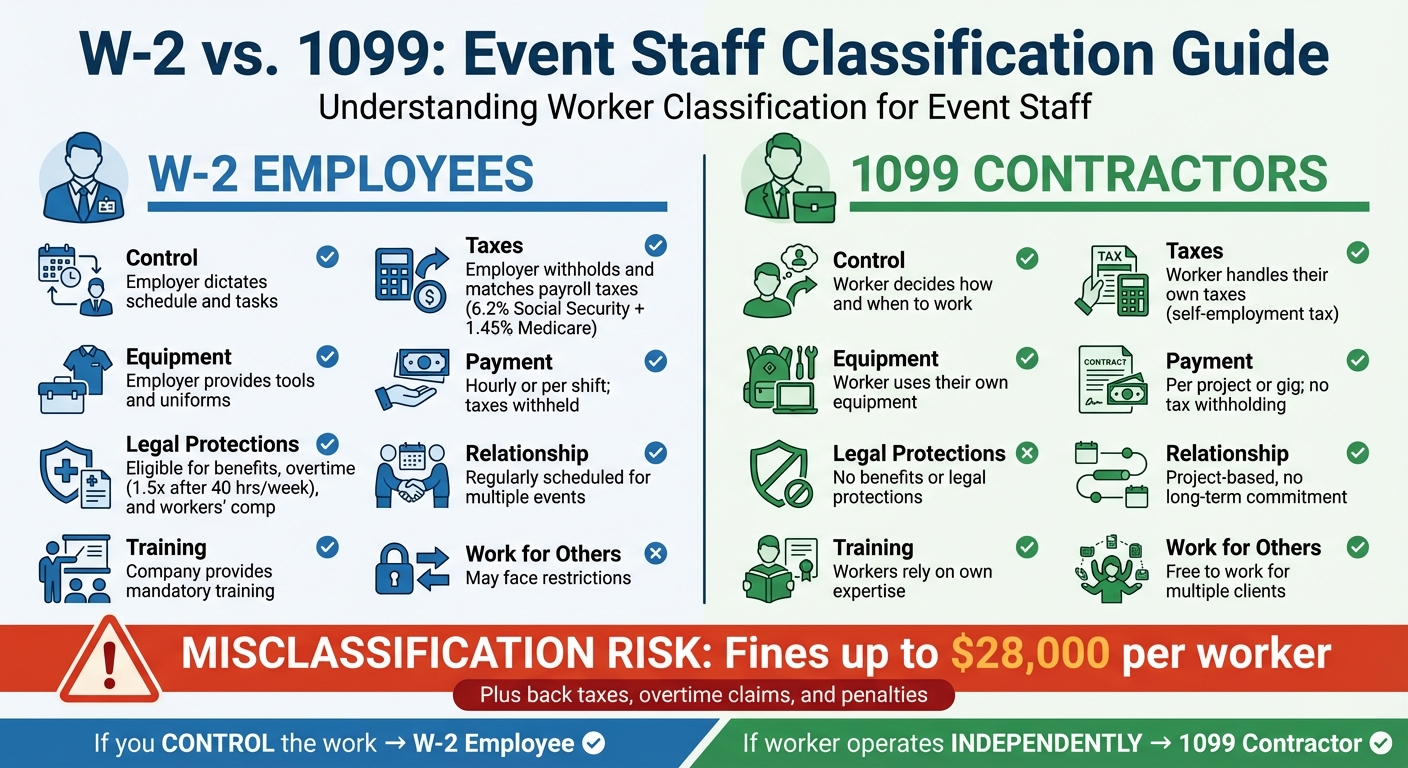

When hiring event staff, the choice between W-2 employees and 1099 contractors impacts taxes, legal obligations, and business operations. Misclassification can lead to audits, fines, and back taxes. Here’s the key difference:

| Criteria | W-2 Employees | 1099 Contractors |

|---|---|---|

| Control | Employer dictates schedule and tasks | Worker decides how and when to work |

| Taxes | Employer withholds and matches payroll taxes | Worker handles their own taxes |

| Equipment | Employer provides tools and uniforms | Worker uses their own equipment |

| Payment | Hourly or per shift; taxes withheld | Per project or gig; no tax withholding |

| Legal Protections | Eligible for benefits, overtime, and workers’ comp | No benefits or legal protections |

Key takeaway: If you control the work, classify as W-2. If the worker operates independently, classify as 1099. Misclassification risks fines up to $28,000 per worker. Use tools like Quickstaff to manage compliance efficiently.

W-2 vs 1099 Worker Classification Comparison for Event Staff

The IRS uses three key factors - behavioral control, financial control, and the type of relationship - to determine whether a worker is classified as an employee (W-2) or an independent contractor (1099).

Behavioral control focuses on how much direction your business gives regarding how work is performed. For example, if you tell a banquet server when to arrive, what uniform to wear, which section to cover, and precisely how to serve, this level of oversight suggests W-2 status. On the other hand, if you hire a freelance photographer for an event who decides their own shooting angles, timing, and assistants, that level of independence aligns more with 1099 classification.

Financial control examines who oversees the business side of the work, such as payment terms, equipment, and the possibility of profit or loss. W-2 employees, like event staff, are typically paid hourly, use company-provided tools, and follow a set schedule. In contrast, 1099 contractors negotiate their rates, supply their own equipment, and often work for multiple clients simultaneously.

The type of relationship looks at the nature and duration of the working arrangement. If you consistently schedule the same servers every weekend, provide benefits, and include them in meetings, this points to W-2 classification. Contractors, however, usually work under specific agreements for individual events, without benefits or deep involvement in the company’s operations.

The Department of Labor (DOL) uses a stricter "economic reality" test, updated in March 2024, to evaluate worker classification. This six-factor test determines whether workers are economically dependent on your business or operate independently. For example, if servers and bartenders are crucial to your operations, and you dictate their schedules and methods, they are likely W-2 employees under both IRS and DOL standards.

Here’s a side-by-side comparison to help clarify classification for event staff:

| Criterion | W-2 Event Staff (Employee) | 1099 Event Staff (Contractor) |

|---|---|---|

| Scheduling Control | Company sets shift times, call times, and breaks. | Workers choose gigs and negotiate schedules. |

| Behavioral Control / Supervision | Tasks are closely supervised, including service methods. | Workers decide how to achieve desired outcomes. |

| Training Requirements | Company provides mandatory training on standards and protocols. | Workers rely on their own expertise with minimal training. |

| Equipment & Uniforms | Company supplies uniforms, tools, and materials. | Workers provide their own tools and attire. |

| Ongoing Relationship | Regularly scheduled for multiple events over time. | Work is project-based with no long-term commitment. |

| Integration into Core Business | Roles like servers and bartenders are central to operations. | Work is more specialized or peripheral to main business functions. |

| Payment Structure | Paid hourly or per shift with taxes withheld. | Paid per project or gig, with no tax withholding. |

| Risk of Profit or Loss | Fixed wages, with most expenses covered by the company. | Profit or loss depends on how workers manage costs. |

| Ability to Work for Others | May face restrictions on working for competitors. | Free to work for multiple clients simultaneously. |

When you hire W-2 event staff, federal and state tax obligations kick in immediately. You’re required to withhold federal income tax from each paycheck based on the employee's Form W-4 selections. On top of that, you must deduct the employee's share of FICA taxes - 6.2% for Social Security (up to the annual wage base) and 1.45% for Medicare on all wages - and match these amounts as the employer.

State income tax withholding is also mandatory in most states, and some cities impose additional local tax requirements. You’ll need to deposit these withholdings on a set schedule and file payroll tax returns for your event staff. By January 31, you’re obligated to issue Form W-2 to each employee who earned at least $600, detailing their total wages, tips, and withheld taxes. Copies of these forms must also be filed with the Social Security Administration and relevant state agencies.

In addition to income tax, you must pay federal unemployment tax (FUTA) and any applicable state unemployment insurance (SUTA) on W-2 wages. Managing these responsibilities can get tricky, especially when juggling multiple events and venues. That’s why many businesses turn to scheduling and payroll tools like Quickstaff, which help track hours, pay, and staff details by event. Tools like this ensure accurate timekeeping and recordkeeping - key for staying on top of W-2 tax compliance.

Before any employee starts a shift, make sure you’ve collected their completed Form W-4 and any state withholding certificates. You’ll also need to complete Form I-9 to verify employment eligibility and maintain time and attendance records for at least three to four years.

Once tax compliance is squared away, the next step is understanding labor law requirements for event staff.

Tax compliance is only part of the equation - labor law standards are just as crucial. Under the Fair Labor Standards Act (FLSA), nonexempt W-2 employees must be paid at least the federal minimum wage of $7.25 per hour and overtime pay at 1.5 times their regular rate for any hours worked over 40 in a week. This applies to common event roles like servers, bartenders, setup crews, and brand ambassadors. Since event schedules often involve long hours and back-to-back shifts, it’s essential to track total weekly hours across all events and locations, as overtime is calculated on a weekly basis, not per event.

Keep in mind that many states and cities have higher minimum wage rates than the federal standard, and some require daily overtime pay (for example, after eight or twelve hours in a single day) in addition to weekly overtime. Certain jurisdictions also mandate paid rest breaks or unpaid meal periods after a set number of hours worked. When federal, state, and local rules differ, you must follow the standard most favorable to the employee. For events spanning multiple cities or counties, be sure to verify the wage and hour rules for each location and include compliance checks in your scheduling and timekeeping processes.

Most states also require employers to provide workers’ compensation insurance for W-2 staff, including event workers handling physically demanding tasks like staging, rigging, and load-in/load-out. If an employee gets injured - whether by lifting heavy equipment or slipping on a wet floor - workers’ comp can cover medical expenses and part of their lost wages. This reduces the risk of facing direct lawsuits. Additionally, you’re required to comply with federal and state safety regulations, including OSHA standards. This involves providing training on safe lifting techniques, equipment usage, crowd management, and emergency procedures. Any workplace incidents should be documented, along with the corrective actions taken.

To avoid common pitfalls, ensure all compensable time - like travel, setup, and tear-down hours - is properly paid. Handle tips according to applicable tip-credit rules and establish clear written policies on compensable time, tip handling, and worker classification. Train managers thoroughly and conduct regular audits of payroll records to catch and address any compliance gaps.

When working with 1099 contractors, their tax obligations differ significantly from those of W‑2 employees. The first step is to collect a completed Form W‑9 from each contractor before issuing any payments. This form captures key details such as the contractor's legal name, business name (if applicable), address, and tax identification number (TIN), which could be a Social Security Number or an Employer Identification Number. While you don’t submit the W‑9 to the IRS, keeping it on file is essential for preparing year-end tax documents.

To ensure smooth tax reporting, keep a detailed record of all payments made to contractors. If a contractor earns $600 or more in a calendar year, you’re required to issue them a Form 1099‑NEC and file it with the IRS by January 31 of the following year. Unlike W‑2 employees, you are not responsible for withholding federal income tax, Social Security, Medicare, or unemployment taxes from their payments. Instead, contractors handle their own self-employment taxes and are expected to make quarterly estimated tax payments.

While this arrangement reduces your payroll tax responsibilities, it places a greater emphasis on accurate bookkeeping. Beyond taxes, maintaining clear boundaries to ensure contractor independence is equally critical for compliance.

A common compliance risk when managing 1099 contractors is exercising too much control over how they perform their work. To maintain compliance, focus on specifying event outcomes - like required hours or dress codes - without dictating daily tasks or methods.

Contractors must have the freedom to manage their own schedules. They should be able to accept or decline specific assignments without facing penalties, work with multiple clients, and use their own tools and equipment. For instance, a freelance bartender who selects which events to work and invoices per event maintains their independent status. On the other hand, assigning fixed shifts similar to those given to W‑2 employees could raise concerns about misclassification.

To reinforce independence, written contracts are essential. These agreements should outline the scope of each project or event, emphasize that the contractor controls how the work is performed, and clarify their responsibility for taxes, insurance, and equipment. Avoid using employee-like terms such as "position" or "supervisor." Instead, describe engagements as on an as-needed basis with mutually agreed rates and timelines. In your day-to-day interactions, focus on providing event-specific requirements - like timing, location, client expectations, or safety protocols - without micromanaging or imposing ongoing supervision.

Digital tools can also help streamline compliance efforts while preserving contractor independence.

"Most staff scheduling software assumes that your staff are employees. Quickstaff ASKS your staff if they are available to work." – Quickstaff

Platforms like Quickstaff make it easier to coordinate with contractors by allowing them to indicate their availability and choose which events to accept. This approach helps you manage logistics while respecting their independence.

Misclassifying workers can lead to hefty financial consequences, especially for businesses in the event industry. If the IRS or the Department of Labor determines that your 1099 contractors should actually be classified as W-2 employees, you could find yourself responsible for unpaid federal and state payroll taxes. This includes both the employer and employee portions of Social Security and Medicare (FICA), federal and state income tax withholding, and unemployment taxes.

The IRS imposes penalties for failure-to-withhold, failure-to-deposit, and inaccuracies, all of which accrue daily compounded interest. State agencies often tack on their own penalties, making the financial burden even heavier. When these liabilities span several years, the total can surpass $28,000 per misclassified worker.

Additionally, you might owe back wages to ensure compliance with minimum wage and overtime laws. Under the Fair Labor Standards Act, overtime - typically 1.5 times the regular hourly rate - must be paid for any hours worked over 40 in a week. The Department of Labor can also assess liquidated damages equal to the unpaid wages and overtime, effectively doubling the amount owed. On top of that, employers may be held accountable for unpaid benefits, such as mandated paid breaks under state law.

Misclassification often triggers audits and investigations from agencies like the IRS, the U.S. Department of Labor, and state workforce or unemployment offices. These reviews scrutinize contracts, payroll records, timesheets, and work schedules to determine whether workers were classified correctly. If reclassified as employees, workers can file individual or class-action lawsuits for unpaid wages, missed breaks, unreimbursed expenses, and denied benefits. In the event and hospitality sectors, class actions involving multiple workers can dramatically increase liabilities, as they often include attorneys' fees and court costs.

These penalties highlight the importance of ensuring proper worker classification before addressing compliant hiring practices.

The financial risks of misclassification aren’t just theoretical - real-world cases from the event industry show how quickly things can escalate.

Take, for instance, overtime disputes involving servers and bartenders. A catering company might classify its servers as contractors while dictating their shifts, requiring attendance at mandatory meetings, and providing uniforms and equipment. If these workers consistently work over 40 hours a week across multiple events, they could later claim overtime as employees. Investigations by the Department of Labor in such cases often result in back overtime payments, liquidated damages, and demands from the IRS for unpaid payroll taxes.

Another common scenario involves setup and tear-down crews. An event production company might rely on a regular team for staging, lighting, and audiovisual work, controlling their schedules and closely supervising their tasks. If these workers are treated as contractors but meet the criteria for employees, a state audit could reclassify them. This reclassification could result in back payments for unemployment insurance, payroll taxes, and wage adjustments for any off-the-clock work.

Even disputes over no-shows, cancellations, and disciplinary actions can expose misclassification issues. For example, penalizing workers for tardiness, enforcing mandatory call times, or withholding pay for last-minute cancellations may demonstrate a level of control that aligns with employee classification under IRS and Department of Labor guidelines. If reclassified, businesses might owe wages for canceled shifts, especially in states with laws requiring minimum guaranteed hours or reporting-time pay, along with back taxes and penalties.

To ensure compliance when hiring event staff, start by classifying each role based on the level of control and independence involved. The IRS and Department of Labor (DOL) provide tests to guide this process. Specifically, use the IRS behavioral, financial, and relationship tests to evaluate each position.

Here’s a simple way to think about it: If you dictate how, when, and where the work gets done - like assigning specific shifts, providing uniforms, and supervising tasks - then the worker is likely a W-2 employee. On the other hand, if you only set deliverables and the worker handles the how - like a freelance DJ who uses their own equipment and determines their own methods - they’re likely a 1099 contractor.

It’s important to document your classification decisions. Keep written contracts that clearly outline the scope of work, payment terms, and level of independence. Job descriptions should also specify the tasks and autonomy tied to the role. During onboarding, make sure to collect the correct tax forms for each worker and document any tools or equipment you provide, as these can impact classification.

Regularly review worker classifications - annually or whenever roles evolve. For example, a bartender who initially worked occasional gigs but now has a regular weekend schedule with assigned shifts may need to be reclassified as an employee. Catching these changes early can save you from penalties down the line.

If you’re unsure about a worker’s classification, consider filing IRS Form SS-8. This form allows you to request an official determination of a worker's status, giving you clear guidance and protecting you from future disputes. By taking these steps, you can ensure that each role is properly defined and compliant with regulations.

Scheduling tools like Quickstaff can play a key role in maintaining compliance. Quickstaff helps you create a clear audit trail by tracking staff availability and event commitments, which is especially useful for supporting 1099 contractor classifications. For example, the platform allows workers to set their own availability and block out dates, reinforcing their independence - an essential factor for contractor status.

For W-2 employees, Quickstaff offers centralized record-keeping to store onboarding documents, contracts, and scheduling logs all in one place. You can upload digital copies of tax forms, track which staff worked specific events, and organize workers by roles to ensure compliance standards are met. This documentation can be critical if your business is ever audited by the IRS or DOL.

"My time spent scheduling has shrunk majorly, leaving me more time to focus on recruiting, onboarding, and training." - Jennifer Manley, Staffing Coordinator

Getting worker classification right comes down to understanding control, taxation, and legal protections. W-2 event staff work under your direction, follow set schedules, and receive benefits. On the other hand, 1099 contractors function as independent businesses, managing their own methods, equipment, and tax responsibilities. The distinction lies in who has control over the work and decision-making.

As highlighted earlier, misclassification is more than just a clerical mistake - it can lead to hefty financial consequences. Misclassifying workers as independent contractors while controlling their work can result in back payroll taxes, overtime claims, interest, and penalties. Both the IRS and the Department of Labor are cracking down, with fines for employment eligibility and misclassification exceeding $28,000 per ineligible hire. For event businesses that rely on seasonal or temporary labor, these costs can escalate quickly.

To minimize risks, follow this rule of thumb: if you're hiring staff to work recurring, scheduled shifts under your direction and as part of your team, they are likely W-2 employees. If you're bringing in specialized professionals for project-based work, who control how they operate and work with multiple clients, a 1099 classification might make more sense. Regularly review worker classifications and ensure contracts and job descriptions clearly reflect their roles.

Digital tools like Quickstaff can simplify compliance by centralizing scheduling and documentation. The platform tracks availability, event assignments, and communication logs, helping you identify whether workers are setting their own schedules (a hallmark of contractors) or adhering to fixed shifts (an employee characteristic). It also provides an audit trail for compliance reviews, ensuring transparency.

Misclassifying event staff as independent contractors (1099) instead of employees (W-2) can cause serious trouble for employers. You could be hit with legal penalties, owe back taxes, and face fines for breaking IRS rules. In some cases, it might even be labeled as payroll fraud.

To steer clear of these problems, it’s crucial to classify your staff correctly. The decision often hinges on factors such as how much control you have over their work, their schedule, and the tools they use. Getting this right not only keeps your business compliant but also shields it from financial and legal headaches.

Determining whether an event worker should be classified as a W-2 employee or a 1099 contractor boils down to how much control you have over their work and how independently they operate. If the worker decides their own schedule, uses their own tools, and takes on projects from multiple clients, they generally fall under the category of a 1099 contractor. However, if you set their working hours, provide the necessary equipment, and dictate how tasks are performed, they’re more likely to be a W-2 employee.

Getting this classification wrong can lead to compliance headaches, including potential fines or penalties. To avoid these issues, take the time to assess the worker’s role thoroughly and consult official guidelines or a professional if you’re unsure about the correct classification.

When bringing W-2 employees on board for event staffing in the U.S., employers must navigate several compliance steps. These include obtaining an Employer Identification Number (EIN), withholding and paying Social Security and Medicare taxes, and securing workers' compensation insurance. Additionally, employers must comply with both federal and state labor laws, such as ensuring adherence to minimum wage and overtime pay standards.

Getting employee classification right is equally important to steer clear of penalties. Unlike independent contractors, W-2 employees are entitled to specific benefits and protections under labor laws. This makes it vital to classify workers accurately and fulfill all related tax and reporting responsibilities.